In the News

This section features the latest news on PAS alongside key capital markets articles and research.

| Apr-25 | Epsilon Launches ETS SaaS: Full-Scale Trade Management, Now in the Cloud

Epsilon is excited to announce the official launch of ETS SaaS, the cloud-native version of its flagship enterprise trade management platform, ETS. With this release, institutional clients can now access the full power of ETS — including complete balance sheet visibility, trade lifecycle management, subledger support, and valuation — without the need to host or manage infrastructure on-premise. |

|

| Mar-25 | PAS: Faster Integration with Python and JMS

Marking another critical milestone in our mission to make the market-proven valuation, risk, and accounting capabilities of the Principia Analytic System (PAS) even more accessible, Epsilon is excited to announce the release of PAS V9.2. |

|

| Aug-24 | Epsilon Introduces TotalCare Managed Service

Epsilon announced the launch of its TotalCare Managed Service, a comprehensive managed service designed to streamline the management of both Epsilon’s ETS and Principia Analytic System (PAS), aimed at optimizing client usage and reducing their administrative burdens. |

|

| May-24 | Epsilon Publishes a RESTful API for the Principia Analytic System

Epsilon has made a significant advancement in their product offerings by launching the Principia Analytic System (PAS) RESTful API with the release of PAS V9.1. This new API exposes PAS's robust valuation, cash flow, and accounting engines, enabling external systems to seamlessly interact with PAS in real time, reducing programmatic complexity and vastly enhancing the accessibility of financial calculations. |

|

| Jan-24 | Epsilon Acquires Principia

Epsilon announced its acquisition of Principia, thereby adding the Principia Analytic System to its product line alongside ETS, a comprehensive and sophisticated trade management platform designed specifically for Federal Home Loan Banks, GSEs, and regional banks. |

|

| Nov-23 | Principia Names Douglas Long CEO

Today we announced the appointment of Dr. Douglas V. Long as Chief Executive Officer. Dr. Long succeeds Theresa L. Adams, who has led the company for over 25 years. Ms. Adams will remain as Chairperson. |

|

| Jul-23 | IOSCO Issues Statement Alternatives to USD LIBOR

The IOSCO issued a statement regarding replacements to USD LIBOR which included warnings about the misuse of Term SOFR and Credit Sensitive Rates. |

|

| Apr-23 | OCC Issues Joint Statement on LIBOR Transition

The Office of the Comptroller of the Currency (OCC) and other federal financial institution regulatory agencies issued a joint statement regarding the LIBOR Transition. |

|

| Apr-23 | FCA Announces Decision on Synthetic USD LIBOR

The FCA has announced that it will compel LIBOR's administrator (ICE) to continue publishing 1-, 3- and 6-month USD LIBOR settings using an unrepresentative 'synthetic' methodology until September 2024. |

|

| Mar-23 | ISDA Updates Guidance on IBOR Fallbacks

Fallbacks seem like a simple replacement rate, but it's not so simple after all. This ISDA guidance gives some of the clearest language to date on the "gotchas" of IBOR Fallbacks. |

|

| Mar-23 | Bloomberg Resources for LIBOR Transition

Bloomberg has a number of helpful fact sheets, guides and rulebooks for managing the LIBOR Transition which they have recently updated. |

|

| Feb-23 | CME Eurodollar Futures Fallback Plans

The CME announced it will convert all eligible Eurodollar futures and options to their SOFR equivalents on April 14, 2023. |

|

| Oct-22 | FASB October Meeting Decisions

The FCA has decided to permanently cease publication of the 1M- and 6M- synthetic GBP LIBOR at the end of March 2023. |

|

| Sep-22 | FCA Announcement Regarding Cessation of 1M- and 6M- GBP LIBOR

The FCA has decided to permanently cease publication of the 1M- and 6M- synthetic GBP LIBOR at the end of March 2023. |

|

| Aug-22 | CME Conversion for USD LIBOR Cleared Swaps

CME has published the methodology for converting cleared USD LIBOR swaps to their SOFR equivalents. The conversion will take place in phases, including "dress rehearsals" beginning in January 2023. |

|

| May-22 | CME Initiative: SOFR First for Options

CME has announced a new market initiative aimed at speeding up adoption and liquidity for SOFR Options in June and July of 2022. |

|

| Apr-22 | ISDA's Latest Review on Transition to RFRs

The latest analysis of the adoption of alternative risk free rates (RFRs) such as SOFR and SONIA is now available. |

|

| Apr-22 | FASB Proposes Updates to Reference Rates Reform Guidance

The FASB has proposed that reference rate relief guidance period be extended and to also consider SOFR Swap Rates as benchmark interest rates. |

|

| Oct-21 | OCC Releases Self-Assessment Tool for Banks: LIBOR Transition

The OCC has updated their Self-Assessment Tool for Banks regarding the LIBOR Transition, to help them evaluate their preparedness for the cession of LIBOR. |

|

| Oct-21 | CFTC Selects November 8 for SOFR First for Non-Linear Derivatives

The Interest Rate Benchmark Reform Subcommittee of the CFTC has voted to select November 8th, 2021 for switching interdealer trading conventions from LIBOR to SOFR for USD non-linear derivatives. | |

| Jun-21 | SOFR First Initiative

The CFTC has officially recommended that interdealer trading conventions should switch to SOFR from July 26, 2021 for linear swaps. |

|

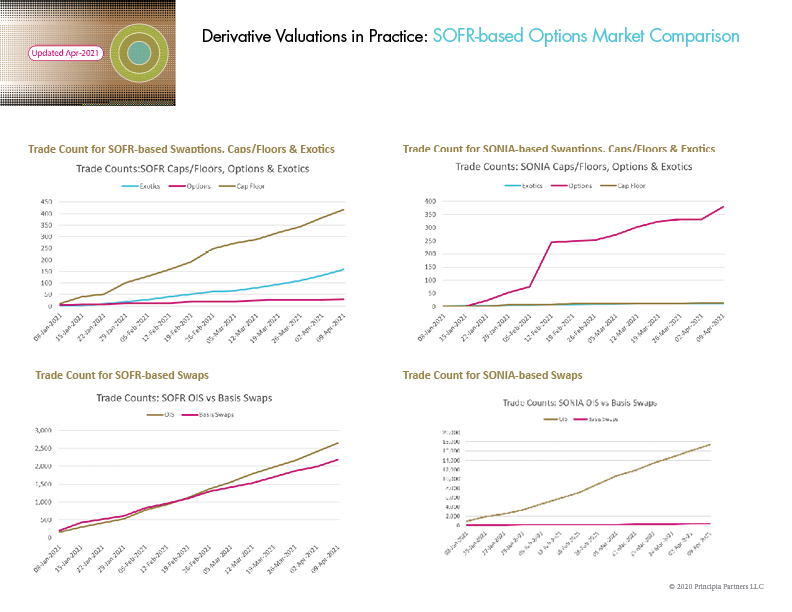

| Apr-21 | Trading Trend for SOFR-based Option Products

At long last, trading volumes for SOFR-based caps and floors seems to be gaining some momentum though other SOFR-based options are picking up at a much slower pace. Comparing these volumes to the SONIA in the UK, it is evident that there is still a very long way to go, however. |

|

| Mar-21 | IBOR Fallback Rule Book and FAQs

In addition to the IBOR Fallback Rate Adjustments Rule Book, published by ISDA and Bloomberg, Bloomberg has recently published a handy set of frequently asked questions on the topic. |

|

| Mar-21 | Progress Report on Transition from USD LIBOR

The Alternative Reference Rates Committee (ARRC) today issued its progress report on the transition away from U.S. Dollar LIBOR. The report came out shortly after announcements from U.S. regulators and LIBOR's administrator, which clarified the end dates for use of USD LIBOR as well as when it will cease publication. |

|

| Nov-20 | The Federal Reserve's Statement on LIBOR Cessation

The transition away from LIBOR got a needed push today when the Federal Reserve Bank and other agencies issued a joint statement warning against the continued use of LIBOR. |

|

| Aug-20 | Principia Announces Early Achievement of SOFR Readiness Targets

Principia announced that both their enterprise platform, Principia Analytic System, and online valuation service, pasVal meet or exceed all SOFR readiness targets as itemized by the ARRC in their Internal Systems & Processes: Transition Aid for SOFR Adoption guide, published in July 2020. |

|

| Jul-20 | TPG to Provide Derivative Valuations via Principia’s pasVal Service

Principia announced a new alliance with TPG, a leading developer of streamlined front-to-back office investment accounting and management software solutions. The offering will provide TPG clients with derivative valuation services via Principia’s online pasVal service. |

|

| Apr-20 | ISDA's Updates for Interest Rate Derivative Trading Activity Q1 2020

ISDA has published it's Q1 2020 review of trading activity for interest rate derivatives. While both IRD traded notional and trade count increased, US dollar-denominated IRS (fixed for floating) decreased by over 5%. |

|

| Mar-20 | NY Fed Publishes SOFR Averages and SOFR Index

The Federal Reserve Bank of New York has begun publication of three daily compounded averages of SOFR (for 30-, 90-, and 180- days) as well as a daily SOFR index to aid those calculating compounded averages over custom time periods. The SOFR Averages and Index data are published here and the calculation methodology details are available here. They will additionally be updating the indicative historical rates for the SOFR Averages and Index to cover the period between October 2019, when they were initially released, through February 2020. |

|

| Mar-20 | Update: SOFR Market Adoption

SOFR basis swaps have begun to overtake SOFR OIS swaps but this seems to be due to traded notional, not trade count. In addition to SOFR futures options now trading on the CME, the first two SOFR Swaptions have also traded. |

|

| Feb-20 | NY Fed to Publish SOFR Averages and SOFR Index

The Federal Reserve Bank of New York announced a proposal to publish three daily compounded averages of SOFR (for 30-, 90-, and 180- days) as well as a daily SOFR index, starting March 2, 2020, to aid those calculating compounded averages over custom time periods. |

|

| Jan-20 | ISDA's Interest Rate Benchmark Review for Q4 and Full Year 2019

Key SOFR-related highlights from ISDA’s Interest Rate Benchmarks Review for 2019 include over 392 billion in traded notional for SOFR swaps and over 193 billion for SOFR basis swaps. SOFR futures saw a jump in open interest at the end of the year to 2.1 trillion from just 0.3 trillion at the beginning of the year. |

|

| Dec-19 | Coming Soon: SOFR Discounting on Interest Rate Swaps

At the close of business on Friday, October 16, 2020, both the CME and LCH are planning to perform a coordinated single-day transition from discounting all cleared USD interest rate swap products with the EFFR to SOFR. This “big-bang” switch is intended to reduce risks and add momentum to the overall market transition away from LIBOR to SOFR. |

|

| Nov-19 | ISDA's Key Trends OTC Derivatives Markets for First Half 2019

ISDA recently published its review of OTC Derivatives Market Trends between 2019, 2018 and the previous 5 years. On the whole, US dollar-denominated trading has increased particularly in the shorter-term contracts. And there was also “a noticeable boost in the share of cleared IRD contracts, as demonstrated by higher IRD notional outstanding with central counterparties (CCPs).” |

|

| Oct-19 | ISDA's Updates for Interest Rate Derivative Trading Activity Q3 2019

ISDA has published it's Q3 2019 review of trading activity for interest rate derivatives. Both IRD traded notional and trade count rose by 28.2% and 33.7% respectively. See review for more details. |

|

| Oct-19 | FHFA Instructs FHLBanks to Begin Transitioning Away from LIBOR

As of March 31, 2020, the FHLBanks should no longer enter into LIBOR-based transactions with maturities past December 31, 2021. |

|

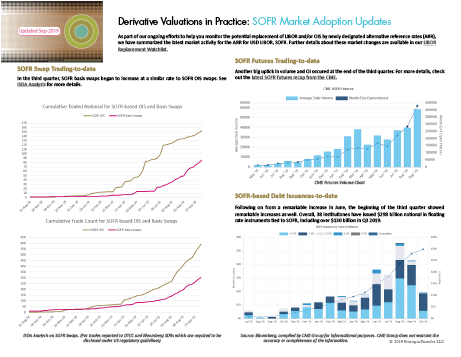

| Sep-19 | Update: SOFR Market Adoption

SOFR-based OIS trading continued strong growth in the third quarter and SOFR basis swaps began to keep pace. |

|

| Sep-19 | Updated Watchlist for LIBOR Replacement

Momentum grows and other markets begin to prepare for the ripple effects of LIBOR replacement. The ARRC has also published a useful matrix comparing current SOFR market conventions. |

|

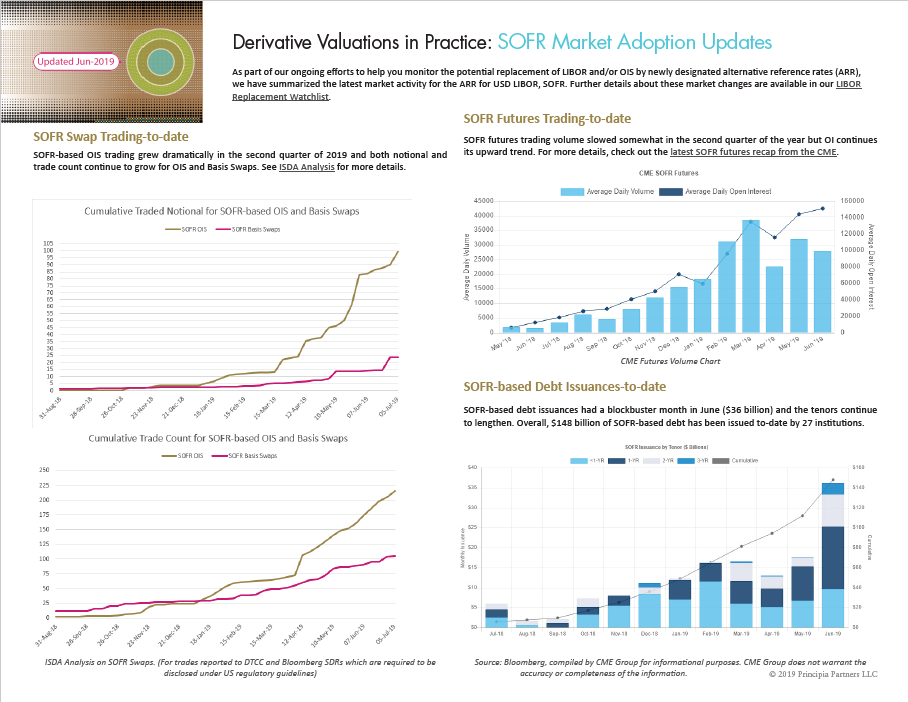

| Jun-19 | Update: SOFR Market Adoption

SOFR-based OIS trading took off at the end of the second quarter and looks likely to continue growth in the third quarter. |

|

| May-19 | FASB ASU 2017-12 Deadline Draws Near

As of December 15, 2018, public companies have been required to implement updates FASB ASU 2017-12 amendment to Topic 815 to their derivatives hedge accounting. |

|

| May-19 | Updated Watchlist for LIBOR Replacement

The CME is supporting discussions around a "big bang" transition to discounting with SOFR instead of EFFR and the ARRC has released recommended fallback language for FRNs and Syndicated Loans. |

|

| May-19 | ISDA's Updates for Interest Rate Derivative Trading Activity Q1 2019

ISDA has published it's Q1 2019 review of trading activity for interest rate derivatives. Both traded notional and trade count rose by 5% and 3.3% respectively. See review for more details. |

|

| Mar-19 | Principia Now Offering a Comprehensive Solution for

SOFR Derivatives Principia has announced the full integration of SOFR into their platform, Principia SFP, and the online derivatives valuation service powered by it, pasVal. |

|

| Mar-19 | Update: SOFR Market Adoption

SOFR issuances, futures, and swaps took off in the new year. |

|

| Mar-19 | Updated Watchlist for LIBOR Replacement

SOFR-based issuance in February 2019 was 25% of total issuance to-date (16.4B out of 65B since July 2018) and CME SOFR futures trading nearly doubled in both volume and open interest from January to February 2019. |

|

| Jan-19 | ISDA's Updates for Interest Rate Derivative Trading Activity Q4 2018

ISDA has published it's Q4 review of trading activity for interest rate derivatives. Both traded notional and trade count rose by 21.9% and 13.5% respectively. See review for more details. |

|

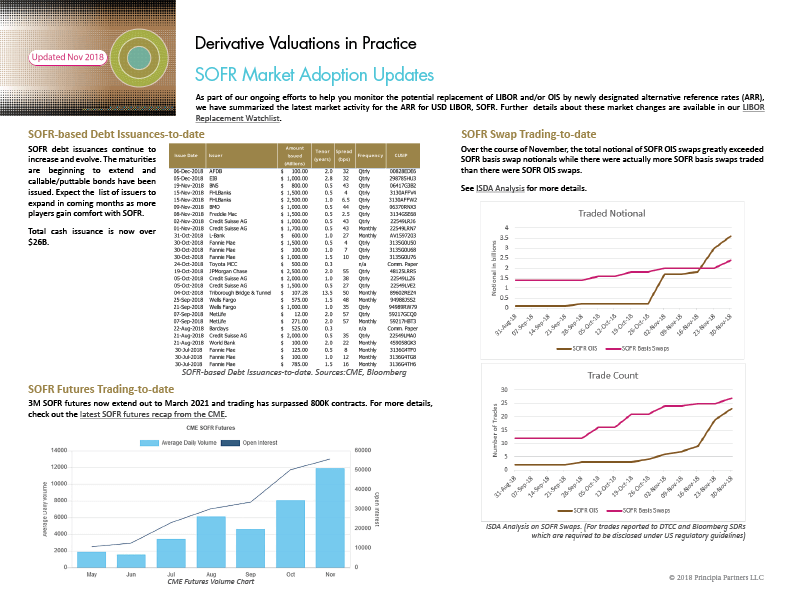

| Dec-18 | Update: SOFR Market Adoption

SOFR issuances, futures, and swaps all significantly increased trading in October and November 2018. |

|

| Nov-18 | Updated Watchlist for LIBOR Replacement

In November, ISDA announced a preliminary fallback methodology while SOFR-based issuances and swaps continued to grow and the ECB discontinued 2W, 2M and 9M tenors of EURIBOR. |

|

| Nov-18 | ISDA's Updates for Interest Rate Derivative Trading Activity Q3 2018 ISDA has published it's Q3 review of trading activity for interest rate derivatives. IRD traded notional and trade count has risen by 14.5% and 7.8% respectively. See review for more details. |

|

| Nov-18 | Principia Offers SOFR Impact Assessments with pasVal

Principia announced its new service: impact assessments for the US market transition away from LIBOR to replacement, SOFR. |

|

| Oct-18 | FASB Issues Accounting Standards Update for New Benchmark

On October 25, 2018 FASB issued an Accounting Standards Update "that expanded the list of U.S. benchmark interest rates permitted in the application of hedge accounting." This update permits the new secured overnight rate, SOFR, to be an allowed benchmark interest rate for hedge accounting (ASC 815). |

|

| Oct-18 | Updated Watchlist for LIBOR Replacement

FASB makes SOFR an eligible benchmark and SOFR swaps are cleared on the CME. |

|

| Sep-18 | Updated Watchlist for LIBOR Replacement

SOFR-based debt issuances and swaps continue to grow, and the ARRC requests consultation for fallback language. |

|

| Sep-18 | SOFR Derivatives Now Available with pasVal Principia announced the launch of its feature set to fully capture and value SOFR derivatives via subscription to their monthly online valuation service, pasVal. |

|

| Aug-18 | Updated Watchlist for LIBOR Replacement

New strides in market acceptance of SOFR with the first debt issuances and swaps entering the market. The pace is picking up - get the latest updates. |

|

| Jul-18 | Updated Watchlist for LIBOR Replacement

ISDA urges immediate action and publishes checklist. SOFR swaps begin trading. Get the latest market developments for replacements to LIBOR. |

|

| May-18 | Updated Watchlist for LIBOR Replacement

SOFR futures have begun trading and SONIA futures will follow in June. Get the latest market developments for replacements to LIBOR. |

|

| Apr-18 | Updated Watchlist for LIBOR Replacement

The proposed USD LIBOR replacement, SOFR, has begun publication and we've updated our watchlist with all the latest news. |

|

| Feb-18 | Updated Watchlist for LIBOR Replacement

We've updated our watchlist with the latest market events related to LIBOR reform and replacement. |

|

| Feb-18 | FASB Proposes Accounting Standards Update for New Benchmark

On February 20, 2018 FASB proposed an Accounting Standards Update "that would expand the list of U.S. benchmark interest rates permitted in the application of hedge accounting." This update would allow the new secured overnight rate, SOFR, to be an allowed benchmark interest rate for hedge accounting (ASC 815). |

|

| Nov-17 | Watchlist for LIBOR Replacement

We've prepared a handy watchlist to help you get ready as alternative benchmarks to LIBOR enter the market. |

|

| Aug-17 | FASB Simplifies Derivatives Hedge Accounting

FASB has announced targeted improvements to hedge accounting requirements for derivatives that will make it easier for many institutions to manage interest rate swaps and improve their risk profiles. They will no longer be required to separately measure and report on effectiveness, changes in hedging item valuations will be shown along with the earnings effect of the hedged item, and it’s easier to use qualitative assessments once an initial quantitative test has passed. |

|

| Feb-16 | GASB 53 Reporting and Effectiveness Testing Made Easy with pasVal

Principia announced GASB 53 reporting and hedge effectiveness tests are now available through its derivatives valuation service, pasVal. |

|

| Dec-15 | Straightforward OIS Discounting Impact Assessment with pasVal

Principia announced OIS discounting impact assessments are now available through its derivatives valuation service, pasVal. |

|

| Oct-15 | Principia Makes Complex Valuations More Accessible With pasVal

Principia announced the launch of its portfolio valuation, risk, and accounting management service, pasVal. |

|

| Jan-15 | Principia Offers New Services for Easier DFAST Reporting

The new service will be available for use in performing DFAST (Dodd-Frank Act Stress Testing) valuations for baseline, adverse, and severely adverse scenarios. |

|